Civil Infrastructure Construction Index

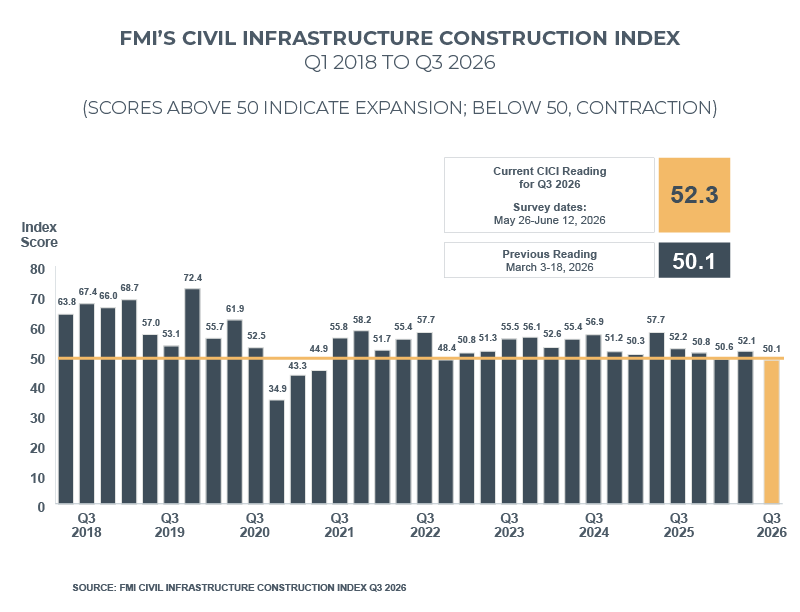

The CICI recovered to 52.3 in Q3 2026 from 50.1 in Q2, reflecting a broad firming in sentiment across civil infrastructure markets.

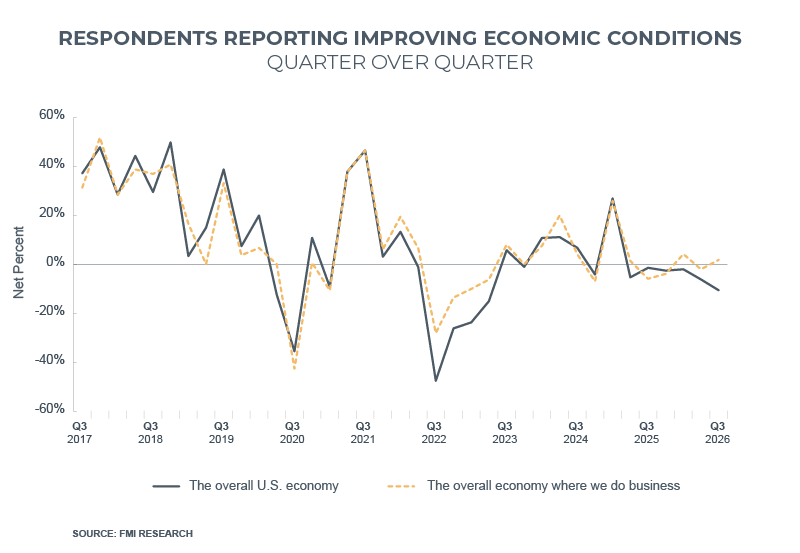

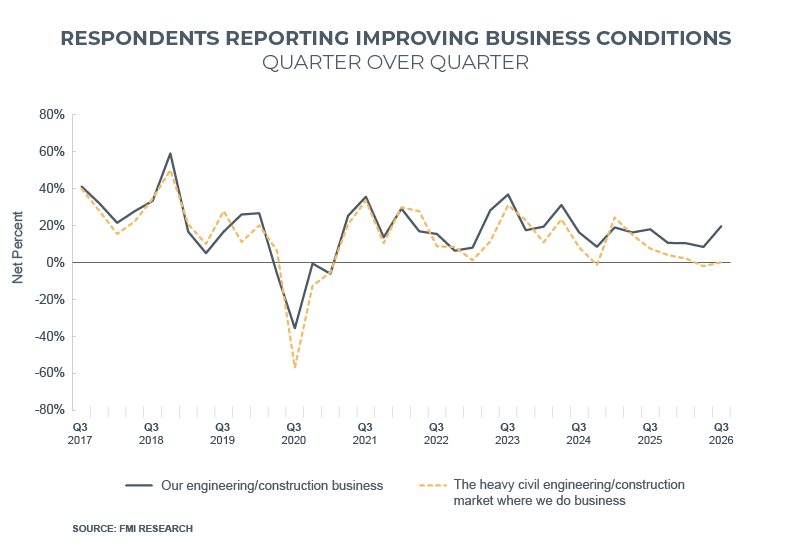

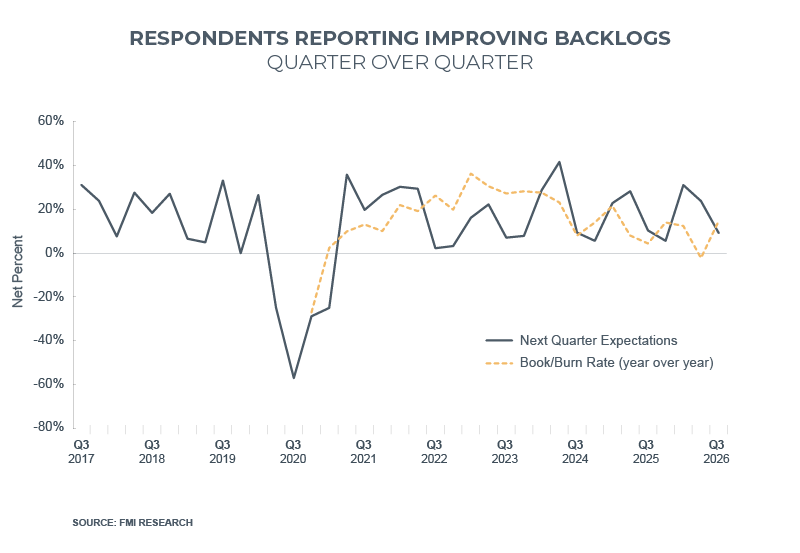

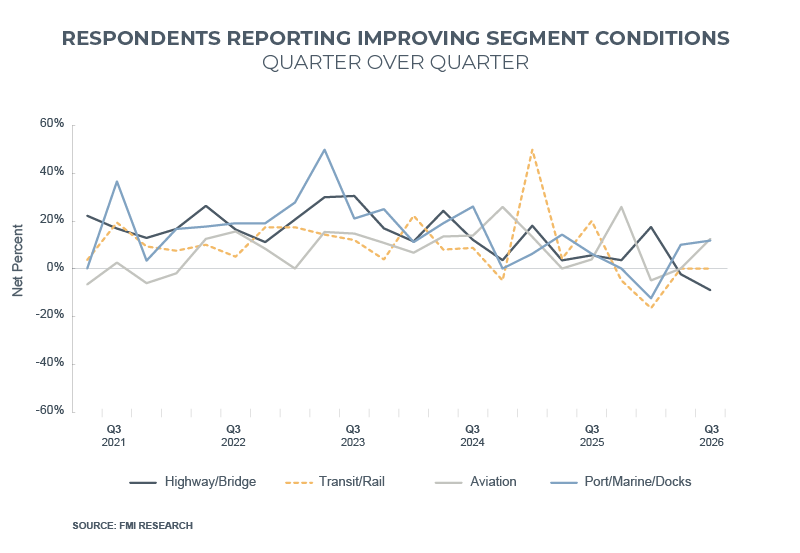

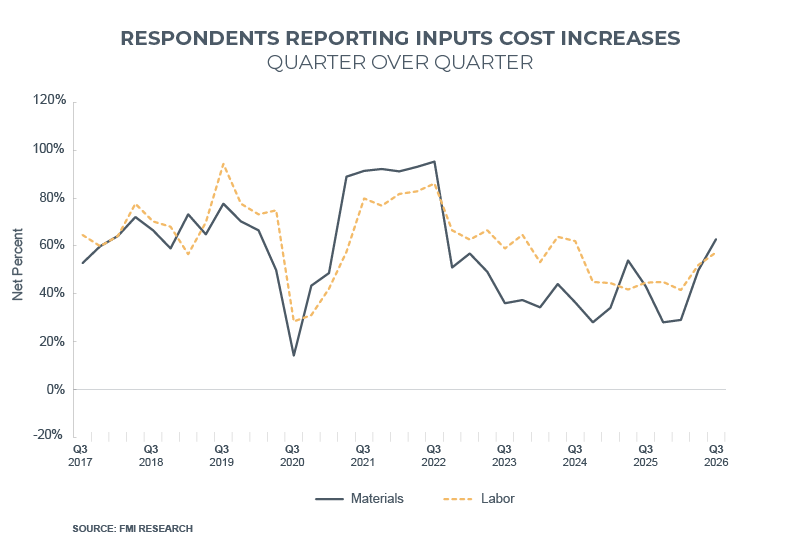

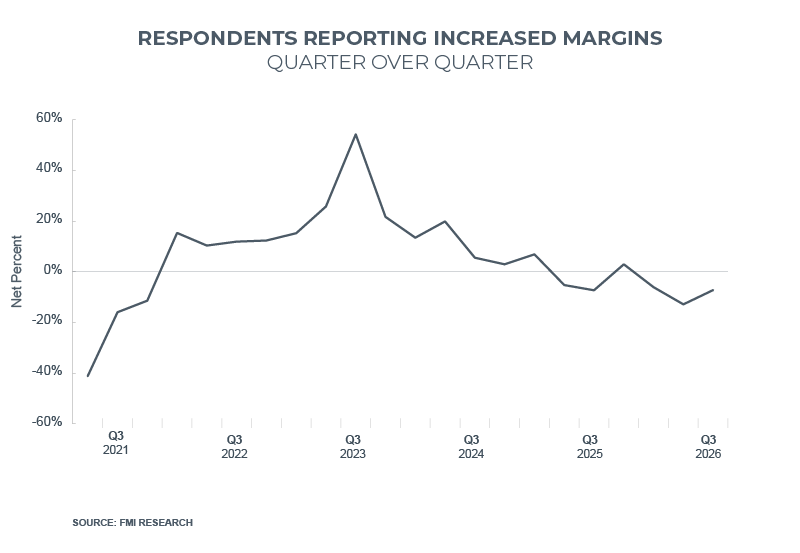

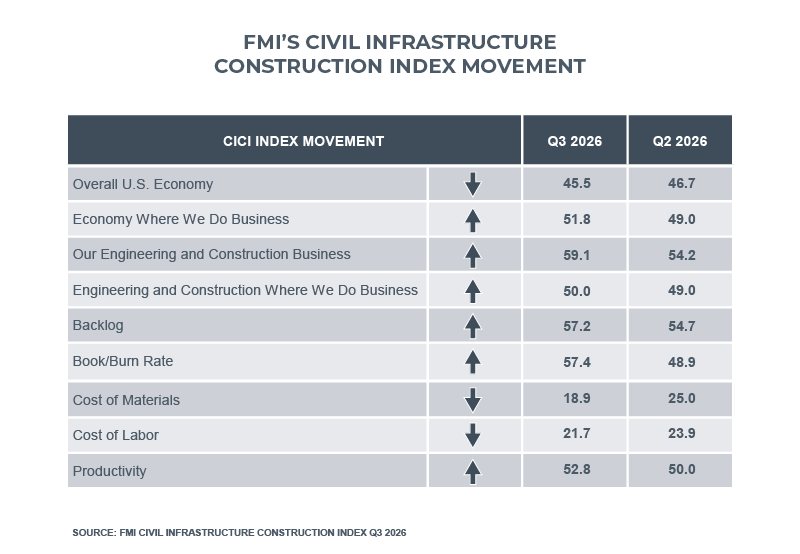

Respondents were mixed on the broader U.S. economy, with views on the overall slipping to 45.5 from 46.7, while sentiment toward the local economies where they operate improved to 51.8, back above the midline. Expectations for their own construction businesses rose to 59.1 from 54.2, as construction conditions in their local markets recovered to the neutral line. Backlog measures strengthened to 57.2 from 54.7, and the book-to-burn rate jumped to 57.4 from 48.9, pointing to refilling pipelines. Cost input readings stayed weak, with materials at 18.9 and labor at 21.7, both well below 50 and signaling broad expectations of further cost escalation. Productivity climbed to 52.8 from 50.0, extending a modest bright spot as crews maintained efficiency despite an uncertain demand outlook.

These index numbers, typically found in the Civil Infrastructure Construction report, are being released as soon as they're available. The full report will be available in the coming weeks. Our survey participants enable us to provide vital insights into current trends and market conditions. If you’re interested in contributing, we encourage you to fill out the CICI sign up form.

The above table and accompanying arrows illustrate how individual components contribute to the overall index score compared to the prior quarter. For most components, scores above 50 signal healthy or expansionary market conditions quarter over quarter. Cost of materials and cost of labor are exceptions whereas lower values in these components indicate expectations for rising prices and serve as a counterbalance.