2025 Civil Infrastructure Construction Index: Third Quarter

The third quarter 2025 Civil Infrastructure Construction Index (CICI) indicates a mix of cautious optimism and emerging challenges for U.S. engineering and construction firms.

FMI’s team of expert consultants works only with companies in the built environment. Our extensive and specialized industry knowledge mean that we’re ready to start helping you improve your business on day one.

All types of contractors across the built environment have engaged FMI to implement tailored solutions for their particular needs, markets and challenges. Contractors leverage our investment banking teams to maximize value when they're looking to grow by acquisition or sell their businesses.

While general contractors and construction managers operate differently, they face many of the same business challenges, such as managing and tracking projects, balancing risk and cash flow, and retaining key talent. Rising material costs, economic uncertainty and the potential for inflation continue to be top of mind for those trying to optimize their businesses and position themselves for growth.

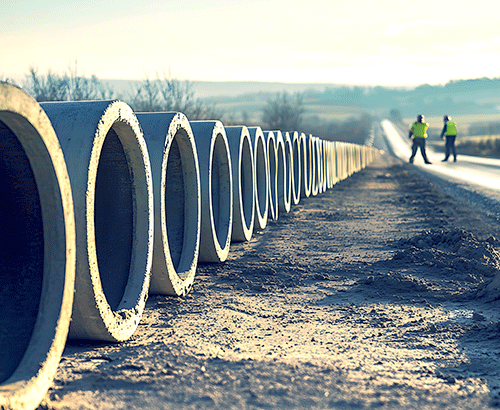

Heavy civil and infrastructure contractors remain one of the strongest sectors of the construction market, particularly as the Infrastructure Investment and Jobs Act (IIJA) continues to drive projects at an accelerated pace. Many heavy civil firms are optimistic about their prospects, with most sectors showing improved expectations. Backlogs continue to grow and margins for heavy civil firms are improving.

That doesn’t mean the path ahead will be easy. Competition continues to increase, and many firms are reaching capacity with labor remaining a large limiting factor. Top risks include the lack of skilled labor, cost increases for materials and equipment, and a potential economic slowdown.

Managing labor productivity, sourcing materials and optimizing equipment are challenges that require focus and discipline. This is particularly true for specialty trades contractors.

Training is not enough to improve performance. A strategic approach to improving direct cost management is imperative for all specialty trade contractors. Additionally, there will also be greater demand for these specialty trade contractors as infrastructure investment increases and competition to complete projects remains high.

Improving the bottom-line profitability begins with superior controls and planning at all levels within the firm.

Capital plans by owners of power, gas and communication infrastructure continue to grow. To fundamentally improve U.S. infrastructure, we need investment that is growing faster than the rate of inflation.

Combining the IIJA, the Inflation Reduction Act (IRA), the Drinking Water and Wastewater Infrastructure Act, and private company investment, the dollars available for repair of utility infrastructure have never higher. The challenge will be finding qualified people to manage and constructe these projects.Leadership and Organizational Development

The third quarter 2025 Civil Infrastructure Construction Index (CICI) indicates a mix of cautious optimism and emerging challenges for U.S. engineering and construction firms.

As the construction industry continues to evolve, more contractors are exploring the opportunity to take on traveling work, or jobs that require them to send crews to new markets. Whether expanding […]

The third quarter 2025 edition of FMI’s North American Engineering and Construction Outlook forecasts just 1% growth in U.S. construction spending. While residential markets face affordability […]

Discover our latest building products sector forecasts, including a deep dive on current flooring trends in the first edition of our 2025 market forecasts.

Our team of experts can help you solve any challenge with specific goals and plans.