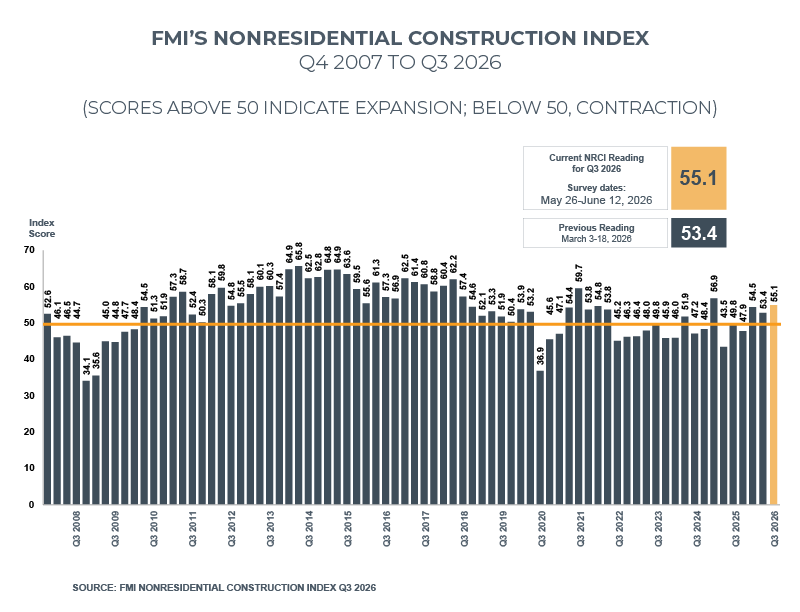

Nonresidential Construction Index

The NRCI rose to 55.1 in Q3 2026, up from 53.4 in Q2, as sentiment firmed across most components and moved the index further into expansion territory.

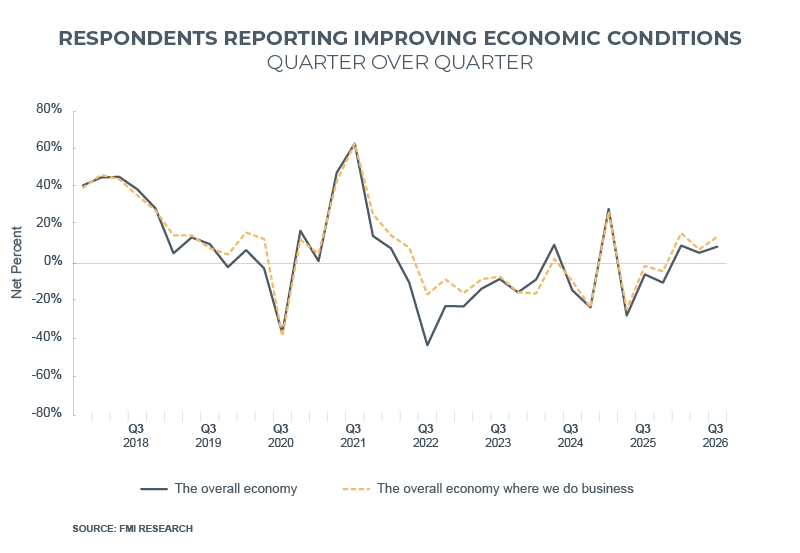

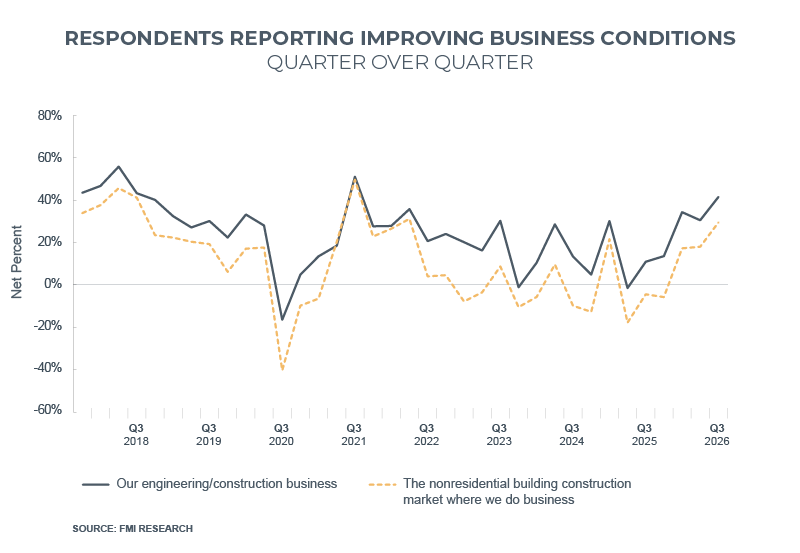

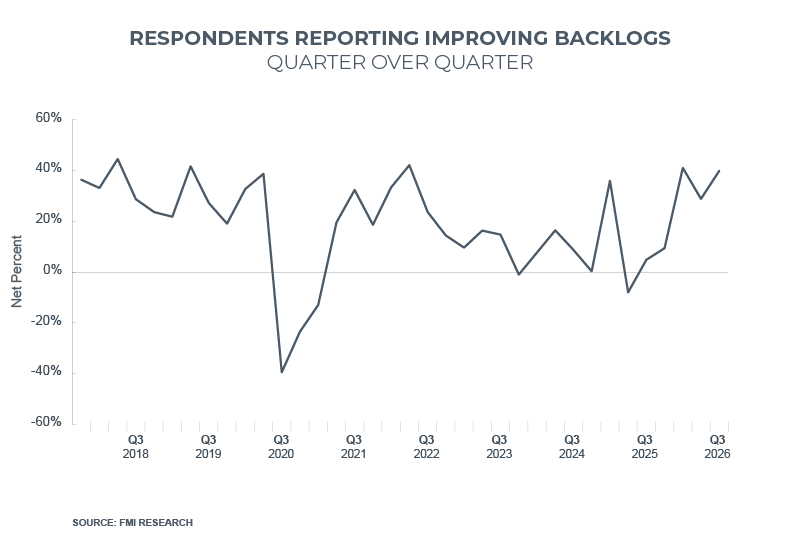

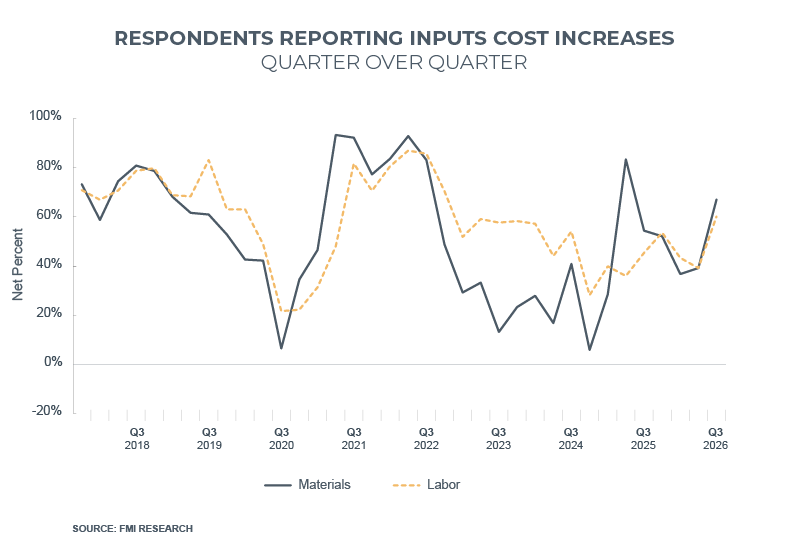

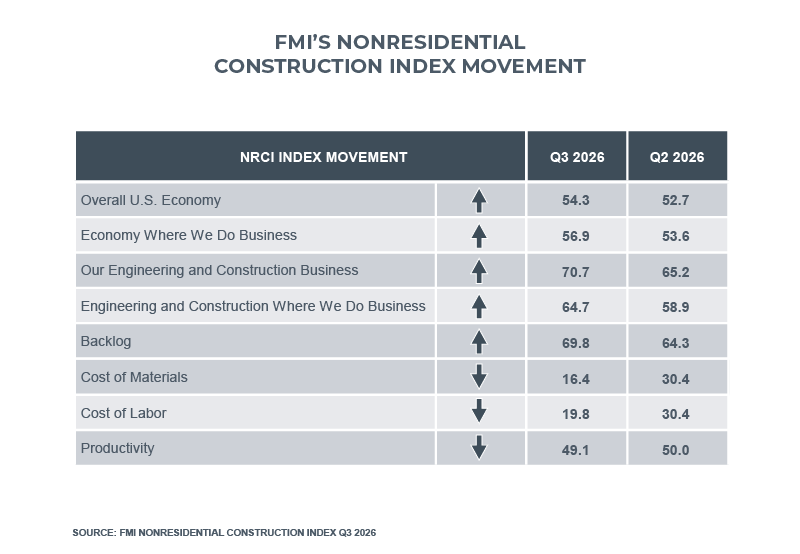

Views on the overall U.S. and the local economies where respondents operate both strengthened to 54.3 and 56.9, respectively, holding comfortably above the midline. Expectations for their own construction businesses remained the strongest component at 70.7, up from 65.2 in Q2, while sentiment toward construction activity in their local markets improved to 64.7. Backlog expectations climbed to 69.8 from 64.3, signaling solid workload visibility into the back half of the year. Cost input readings fell sharply, with materials at 16.4 and labor at 19.8, both well below 50.0 and signaling broad expectations of further cost escalation. Lastly, productivity dipped just below the neutral line to 49.1 as efficiency gains proved hard to sustain.

This index, typically found in the North American Engineering and Construction Outlook report, is being published as soon as it’s available. The full report will be released in the coming weeks. Our survey participants enable us to provide vital insights into current trends and market conditions. If you’re interested in contributing, we encourage you to fill out the NRCI sign up form.

The above table and accompanying arrows illustrate how individual components contribute to the overall index score compared to the prior quarter. For most components, scores above 50 signal healthy or expansionary market conditions quarter over quarter. Cost of materials and cost of labor are exceptions whereas lower values in these components indicate expectations for rising prices and serve as a counterbalance.