The AI Infrastructure Shift: What Recent Public Earnings Signal for ITAD Businesses

The IT Asset Disposition (ITAD) sector is undergoing a structural transformation. For years, the industry operated as a fragmented network of regional e-waste processors. Today, it is a strategic, high-growth sector at the center of AI infrastructure deployment, commanding the attention of global consolidators and private equity sponsors.

If you want proof of this shift, look no further than the earnings reports released February 2026 from two of the industry's largest public players: Iron Mountain (NYSE: IRM) and Sims Limited (ASX: SGM). Their financial results tell a clear story about where the market is heading and how independent operators can maximize their value in this evolving landscape.

Unprecedented Sector Growth

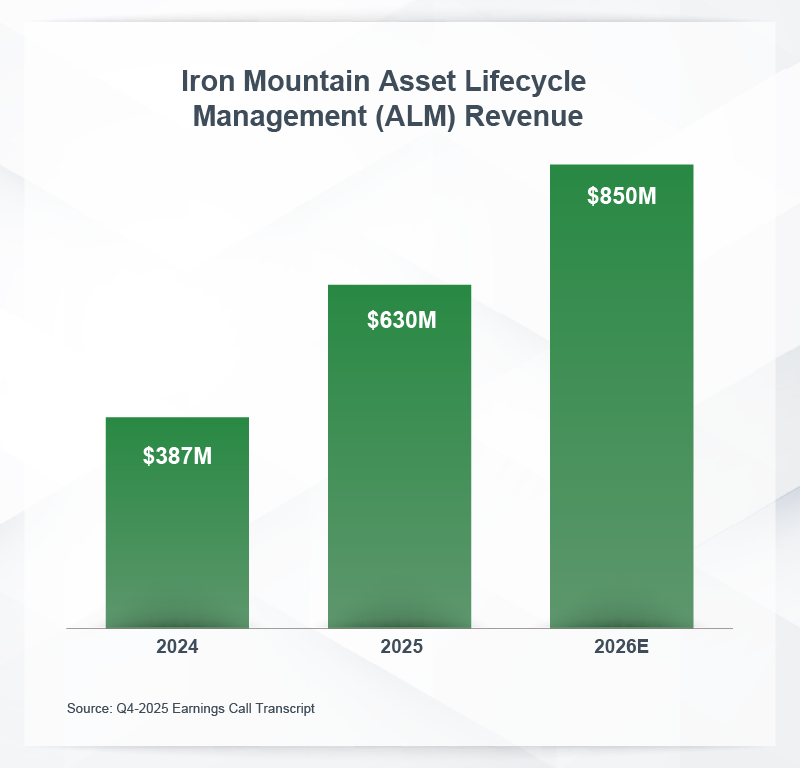

Iron Mountain’s transition from a physical storage player into a diversified ITAD sector leader is accelerating. In its full-year 2025 earnings, the company reported that its Asset Lifecycle Management (ALM) division increased revenue by an astonishing 63%. This is not just a cyclical bump, Iron Mountain is forecasting ALM to become a multi-billion-dollar standalone division. As the data illustrates, the trajectory is staggering. With February 2026 guidance projecting $850 million in ALM revenue for 2026, Iron Mountain is capitalizing on the favorable market environment and its ability to cross-sell ITAD services to its legacy Fortune 1000 storage clients.

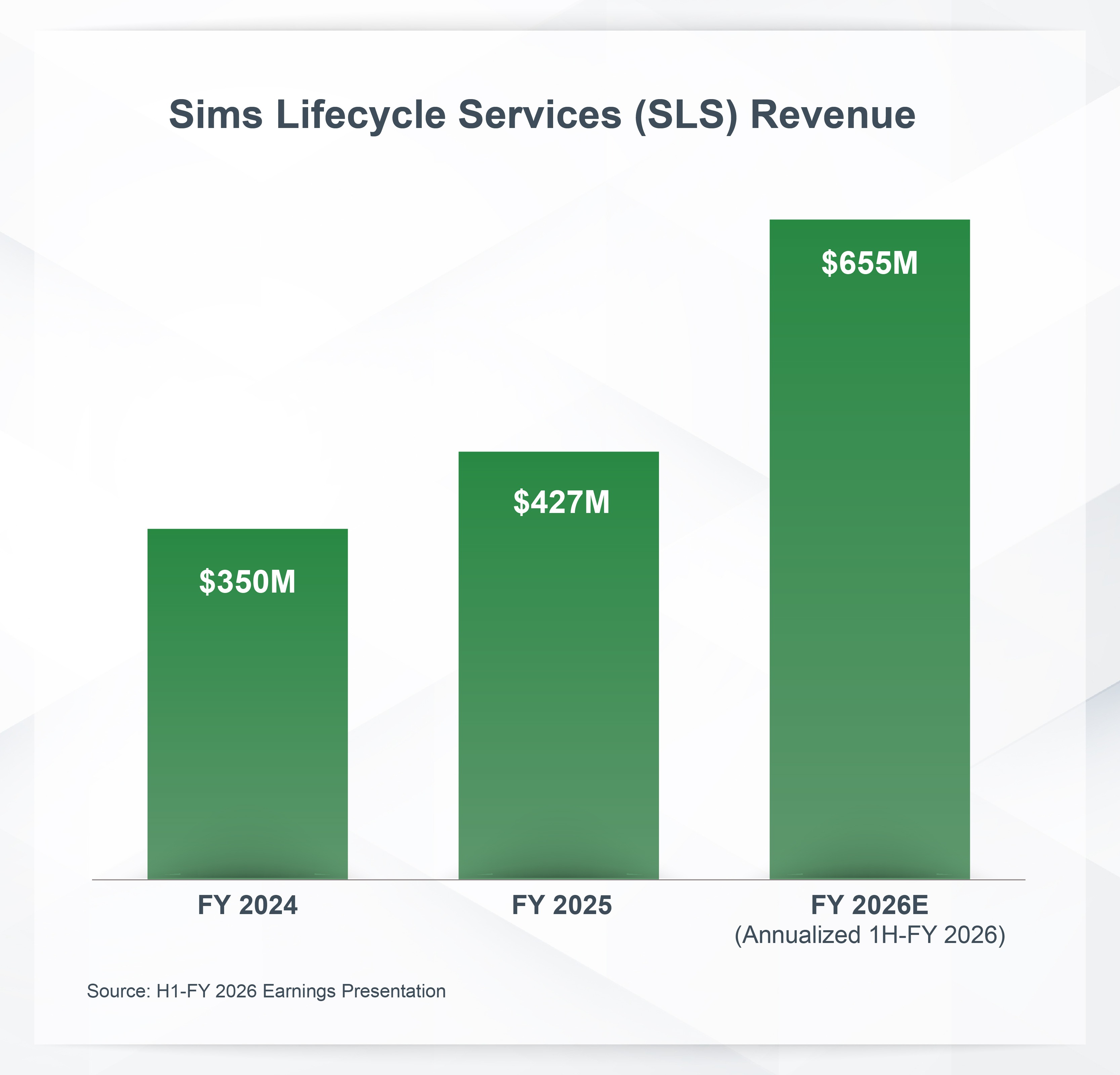

Sims Limited reported a similar acceleration within its ITAD division, Sims Lifecycle Services (SLS). Despite broader macroeconomic headwinds in its traditional ferrous scrap markets, SLS revenue skyrocketed by nearly 70% year over year in the first half of fiscal 2026. A massive driver of Sims' outperformance was the secondary market for components — specifically double data rate 4 (DDR4) memory chips, where pricing surged more than 450% year over year.

The AI Hardware Supercycle

What is driving these unprecedented numbers? The answer lies in the trillion-dollar buildout of AI infrastructure.

As global memory manufacturers pivot their fabrication capacity to produce High Bandwidth Memory (HBM) and DDR5 for new AI infrastructure, the production of standard DDR4 memory has fallen substantially. Yet DDR4 remains the operational workhorse for standard enterprise IT and legacy data center infrastructure.

This dynamic has created a severe supply-demand imbalance. High-quality, repurposed components extracted by ITADs are commanding massive premiums. Sims repurposed 5.3 million units in the first half of fiscal year 2026, underscoring that operators with the scale and technical capability to handle hyperscale decommissioning are reaping the rewards of this secondary market boom.

What This Means for ITAD Founders

For founders and CEOs of independent ITAD platforms, these public earnings provide important market color:

- Beware the "COVID Laptop" Effect on Valuations: While the 450% surge in DDR4 pricing is driving record margins, sophisticated buyers will not pay a peak premium on earnings inflated solely by component pricing. We experienced this exact dynamic during the COVID-19 work-from-home mandate. When used laptop prices temporarily skyrocketed, smart acquirers underwrote deals using a "through-the-cycle" or Last 24 Months (L24M) average to avoid overpaying for a cyclical high.

While the AI infrastructure buildout is more structural, buyers remain cautious about over-valuing component pricing arbitrage. This is why ITAD platforms that have transitioned to a fixed-fee service model command a higher valuation multiple than those relying on percentage-based revenue shares of asset prices. This premium is amplified for operators successfully evolving beyond end-of-life processing to expand upstream into full-lifecycle services and Third Party Maintenance (TPM). Right now, pure-play TPMs that signed fixed-price service agreements before the recent component cost spikes are in a tough spot, as many are unable to pass cost increases through to their clients. Integrated TPM platforms with ITAD capabilities have a structural advantage: a captive, internal supply of high-quality repurposed components that insulates them from spot market volatility.

- Buyer Landscape is Nuanced and Public Strategics Aren't Always the Highest Bidders: During its earnings call, Iron Mountain explicitly stated its acquisition targets trade at "mid- to high-single digits as a multiple of EBITDA." Because of their immense scale, public consolidators see nearly every ITAD platform that comes to market. While their strategy of buying at single-digit multiples is paying off — noting that recent ITAD acquisitions Premier Surplus and ACT Logistics contributed $14 million to the fourth quarter of 2025 revenue alone — they are rarely the ones paying the highest premium. Well-capitalized private equity sponsors and mid-market strategics are actively stretching multiples for the right platforms. Maximizing valuation requires running a competitive process that pits different buyer motivations and capital structures against one another.

- Full Lifecycle and Recurring Revenue Drive Premium Valuations: Strategic buyers and PE sponsors are not looking to acquire volatile, spot-market brokerage businesses. They are hunting for closed-loop ecosystems. The highest M&A multiples are being awarded to platforms that bridge the gap between forward deployment, ongoing TPM and secure decommissioning. Given the margin squeeze currently facing standalone TPMs, buyers place a premium on platforms where ITAD acts as a strategic sourcing engine, feeding cost-effective, repurposed parts directly into the TPM division. Whether it is securing TPM contracts or capturing predictable enterprise lease-return volume, an M&A premium is awarded to operators that lock in exclusive, recurring customer relationships.

Positioning for the Current Cycle

The ITAD sector's flight to quality is underway. Buyers have capital, and the AI-driven hardware deployment is creating a steady flow of high-value decommissioning projects in the data center landscape. These benefits are cascading beyond data centers into enterprise and end-user computing, largely driven by record memory prices. Navigating this structural transition requires positioning your business not as a regional recycler, but as a highly secure, strategic partner in the technology lifecycle.

If you are evaluating growth capital, strategic partnerships or an eventual exit, now is an opportune time to assess how your platform would be viewed in today’s buyer landscape. We are actively advising ITAD and broader asset lifecycle businesses on M&A strategy and valuation positioning and are always happy to have a conversation about the market.

Brett Robinson is a Managing Director with FMI Capital Advisors. He can be reached at [email protected].