From Concrete to Silicon: What Data Center Construction Tells Us About the Future of ITAD

The artificial intelligence boom is not just a software story. It is a physical infrastructure story unfolding at unprecedented scale.

At FMI, our position within the built environment provides us with a unique, forward-looking lens into the future of technology hardware. By tracking where data centers are being built today, we are able to forecast the volume, geography and technical complexity of the IT Asset Disposition (ITAD) market over the next decade.

For the ITAD sector, the current surge in activity is just the precursor. The true wave of exponential growth will occur when today’s massive AI factories inevitably become the feedstock for tomorrow’s secondary market.

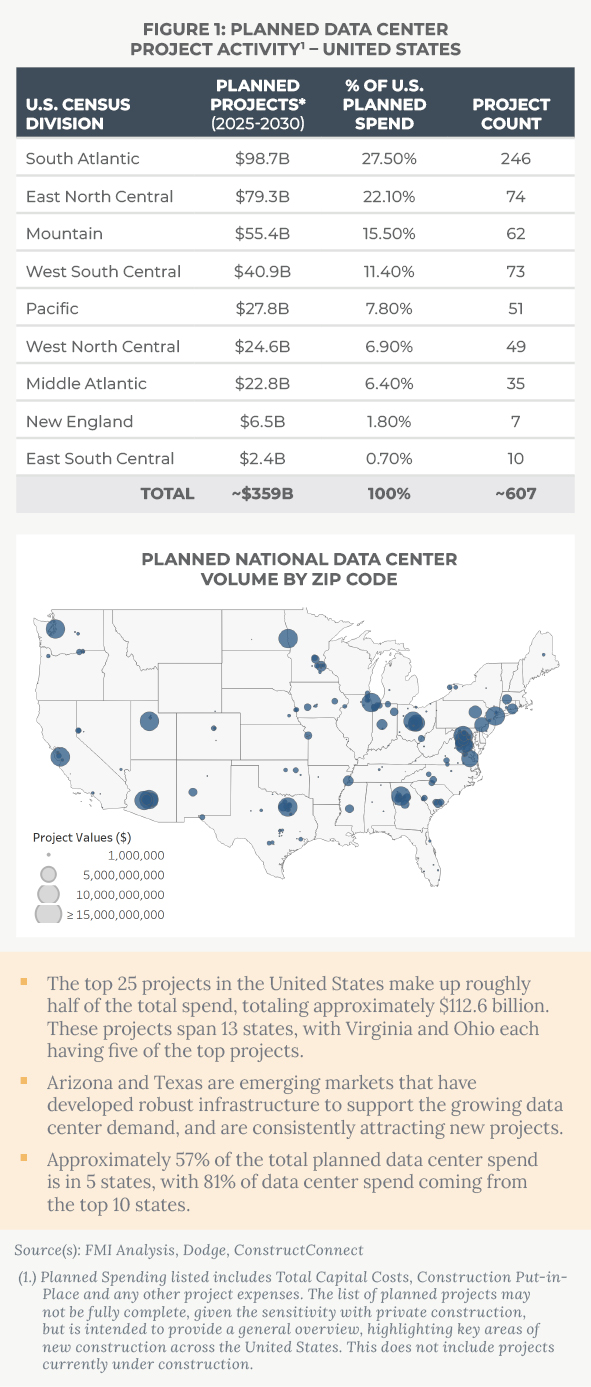

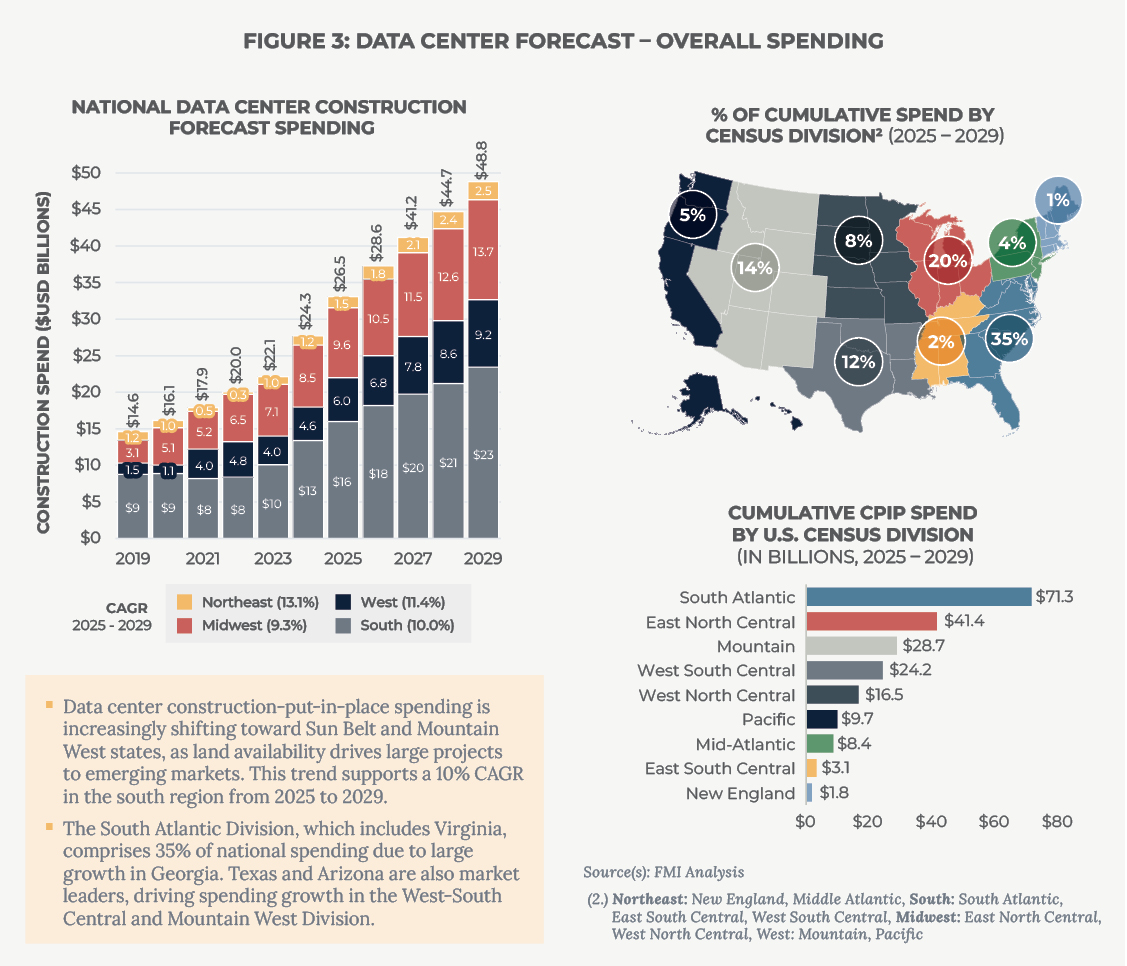

Based on FMI’s tracking of over 600 planned U.S. data center projects, we estimate approximately $359 billion in construction put-in-place, slated through 2030. As illustrated in Figure 1, this massive capital deployment is concentrated geographically, with 81% of the total planned spend occurring in just 10 states.

It is critical to note that this figure accounts strictly for the physical infrastructure. The capital deployed for the actual compute — the high-density servers housed inside — is projected to reach the trillions, with hyperscalers guiding investors to over $600 billion* in capital expenditures (capex) this year alone.

Crucially, the hardware emerging from these facilities will look fundamentally different than legacy enterprise IT. To support 50-100 kW rack densities, hyperscalers are universally adopting direct-to-chip liquid cooling and advanced thermal management systems. Disassembling, sanitizing and remarketing these dense, liquid-filled racks requires highly specialized engineering workflows, hazardous material handling and institutional grade facilities.

The influx of high-value infrastructure represents a critical inflection point for the market. Historically, ITADs easily won business because end-of-life disposition was an administrative afterthought for enterprise clients. Today, AI compute is the core engine of their businesses. Given the immense residual value and technical complexity of these assets, hyperscalers will self-perform their own decommissioning if the external market cannot offer a superior solution at the required volume and precision. Because hyperscalers will refuse to hand over their multimillion-dollar AI racks to subscale, undercapitalized operators, the industry is experiencing both a surge in quality and a race for scale.

The Throughput Demands Reshaping the Mid-Market ITAD Model

New data center construction represents a structural opportunity that will redefine the current ITAD operating model. Today, a successful mid-market ITAD operates out of a 50,000-square-foot warehouse, optimized for a predictable volume of legacy enterprise hardware.

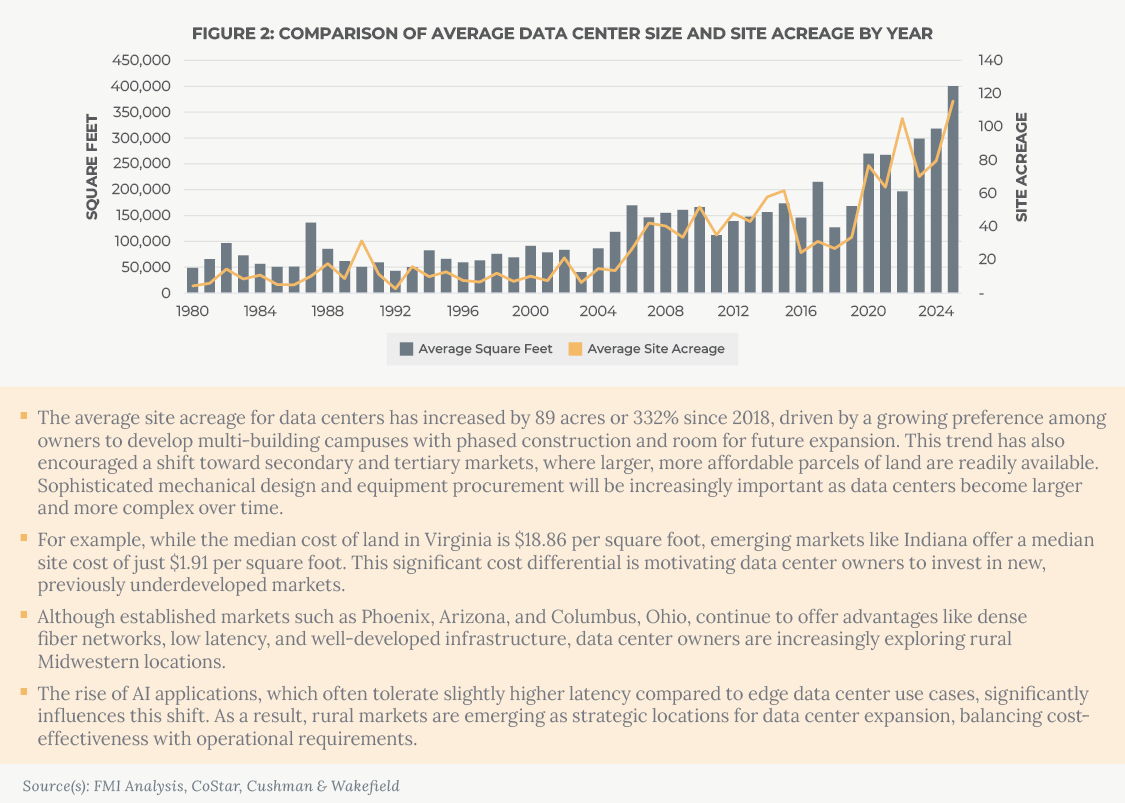

That footprint physically cannot scale to absorb the mega-campuses being built today. FMI’s tracking reveals that average data center site acreage has exploded by 332% since 2018, with average building footprints now pushing toward 400,000 square feet.

When a hyperscaler decommissions one of these modern, sprawling mega-campuses, it does not trickle the hardware out over 12 months. To minimize downtime and clear floor space for the next generation of compute, the facility must be purged rapidly. This means tens of thousands of high-density servers, network switches and heavily engineered racks hitting the reverse supply chain in a highly condensed, multi-month sprint.

For the ITAD sector, this shifts the competitive environment from sales-centric relationships to throughput capacity and facility capex. You cannot push a 400,000-square-foot data center refresh through a 50,000-square-foot ITAD warehouse. Absorbing a hyperscale refresh requires an entirely different class of infrastructure.

An ITAD platform must possess:

- Larger Facility Footprints: Facilities over 150,000 square feet are capable of staging multiple inbound truckloads simultaneously, without causing bottlenecks at the loading docks.

- Working Capital and Balance Sheet Strength: Processing, testing and remarketing thousands of advanced GPUs takes time. The ITAD must have the balance sheet to float the immense operational costs and working capital required, all while the hardware works its way through the disposition and resale channels.

The sheer tonnage of the AI hardware lifecycle dictates that ITADs with larger facilities will be best positioned for success.

The Geographic Migration of Compute Infrastructure

For the last decade, the geography of the data center ITAD market was relatively straightforward. If an operator maintained a processing facility near “Data Center Alley” in Virginia, they were positioned to capture a massive share of the nation’s end-of-life hardware.

The power demands of artificial intelligence have changed this.

The electrical grids and land availability in legacy hubs are constrained, forcing infrastructure developers to look elsewhere. FMI’s tracking of the built environment reveals a geographic migration. While Northern Virginia remains a critical hub, Georgia, Texas, Arizona and the Midwest are also market leaders.

Phoenix is preparing to host massive infrastructure investments, such as the planned $20 billion Tract Data Center Complex. Similarly, markets like Dallas, Texas; Atlanta, Georgia; Columbus, Ohio; and Northern Indiana are rapidly becoming the new epicenters of national compute power.

In ITAD, geography is critical because reverse logistics significantly impact margins. Shipping 3,000-pound, liquid-cooled AI racks across the country is inefficient. Furthermore, hyperscalers view distance as a security liability. Demanding an airtight chain of custody, they will naturally prioritize localized processing over multiday transits.

To win the national hyperscale contracts of tomorrow, an ITAD platform must have processing facilities geographically aligned with the concrete being poured today.

The Technical Complexity of AI Decommissioning

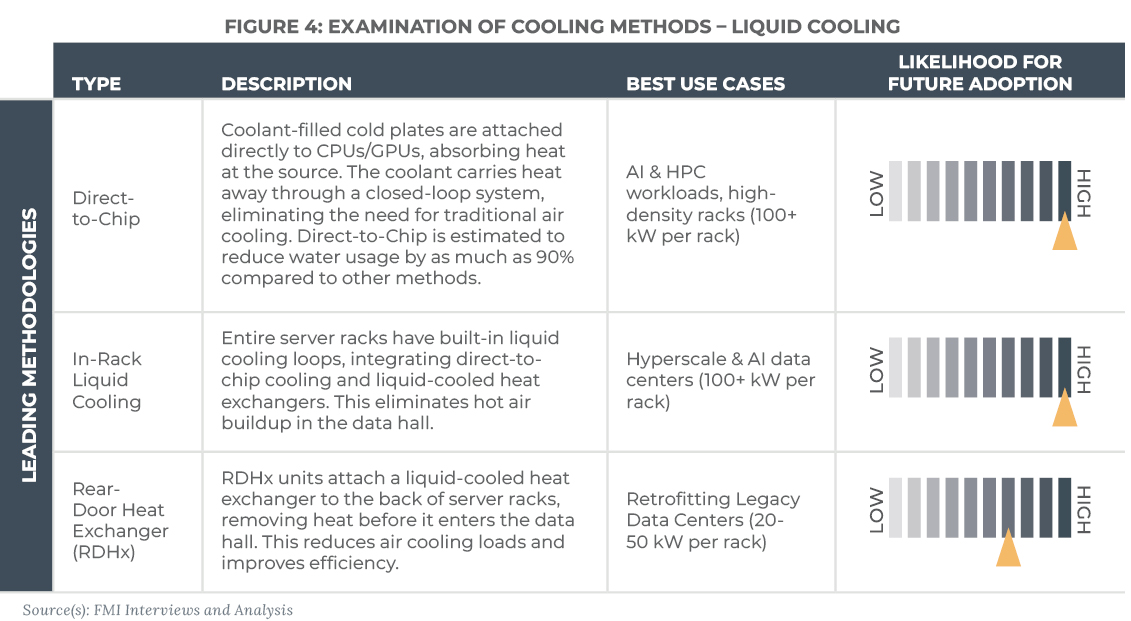

Beyond volume and geography, the physical architecture of AI infrastructure will rapidly outpace the capabilities of traditional ITAD facilities. Because AI workloads push rack power densities to 100 kW and beyond, hyperscalers are abandoning traditional air cooling. As detailed in our examination of cooling methodologies in Figure 4 below, direct-to-chip and in-rack liquid cooling systems have the highest likelihood of future adoption for these advanced AI workloads, outpacing retrofit solutions like rear-door heat exchangers.

For the ITAD market, this represents an actionable insight: the assets arriving at loading docks in the coming years will be exponentially more complex than those in today’s secondary market.

The legacy workflow of manually un-racking standard, air-cooled 1U servers is no longer sufficient for the AI era. Processing this incoming wave of liquid-cooled infrastructure introduces entirely new, technically demanding engineering hurdles:

- Structural Density and Weight: Fully loaded AI racks weigh thousands of pounds. Some warehouse floor-load capacities, loading docks and lifts may not be structurally engineered to safely offload or maneuver these massive units.

- Environmental Stewardship and Component Integrity: While initial bulk-draining often occurs on-site, the ITAD platform must possess specialized fluid-management workflows to handle residual coolants and perform the precision cleaning required to preserve the secondary market value of the silicon.

- Technical Component Recovery: Harvesting Blackwell-series or next-generation GPUs from liquid-cooled manifolds requires a high-precision disassembly environment. Standard manual teardown processes are insufficient for these fragile, high-value assets.

Today, the majority of the 500-plus independent operators in the U.S. ITAD market lack the research and development budgets, the specialized engineering talent and the facility infrastructure to handle complex thermal decommissioning. When hyperscalers issue requests for proposals to decommission these mega-campuses, they will audit prospective ITAD partners for these specific capabilities.

Conclusion

FMI’s analysis of the data-center built environment provides a roadmap for the ITAD market over the next decade. By tracking the 600 projects and $359 billion in planned construction today, we can forecast the volume, geography and technical sophistication required of ITAD platforms in the future.

The ITAD market is already benefiting from a legacy retrofit cycle, as data center operators purge decades of air-cooled enterprise hardware to clear floor space for high-density AI clusters. This “rip and replace” activity is providing a robust, high-volume baseline for the industry today.

The more significant opportunity, however, lies ahead. As the ~600 mega-scale data centers currently planned or under construction begin their first refresh cycles, the industry will face a step-change in both volume and complexity.

The competitive landscape is already shifting toward larger, better-capitalized operators capable of meeting these demands. As hyperscalers place greater emphasis on security, speed and technical precision, they will increasingly concentrate volume among partners that can operate at scale or internalize the function altogether.

Ultimately, the concrete being poured today will define the ITAD market over the next decade. The firms positioned to win in the future will be those building now, at the right scale, in the right locations and with the technical sophistication to process the next generation of AI infrastructure.